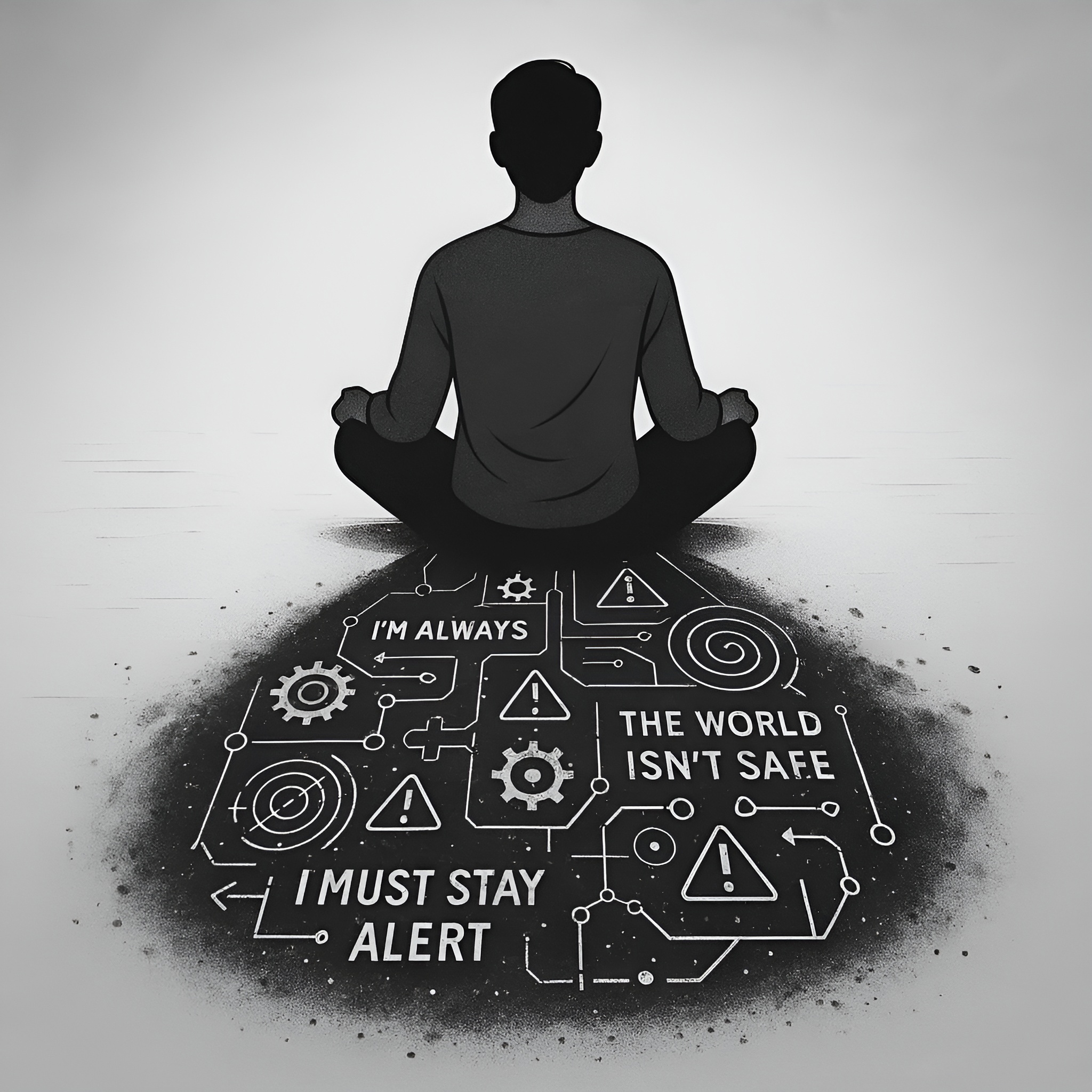

Money stress isn’t really about money.

It’s about beliefs—identity-level beliefs—running the show underneath.

In this episode, Andrea McTague sits down with Jenae White (Registered Provisional Psychologist at our Calgary studio) and Crystal Taylor (Licensed Financial Advisor and She-EO of Holden + Taylor Advisory Group) to break down why Calgarians get stuck in cycles of overspending, shutting down, avoidance, guilt, shame, and never feeling “ahead.”

They uncover the beliefs that quietly drive financial anxiety and the nervous-system patterns that keep people looping—no matter how much they earn.

If you’re in Calgary and this episode hits close to home, especially around stress, pressure, or money anxiety. You can explore how structured, evidence-based therapy works at the identity level here:

👉 Calgary Therapy: What Most People Don’t Know When Choosing a Psychologist

This is our main Calgary guide that breaks down what to look for, what actually matters, and why most people don’t get the clarity they deserve before starting therapy.

Table of Contents

🎧 Episode Summary

Whether you’re a white-knuckle budgeter, an avoidance spender, or someone who freezes the moment your banking app opens, this episode reframes money stress in a way most people never hear.

Yes — discipline matters.

And yes — financial literacy matters.

But conscious knowledge can’t override unconscious threat responses.

You can know exactly what you “should” be doing.

You can be smart, capable, and logically aware that your strategy makes sense.

And still:

- overspend

- avoid statements

- panic-plan

- shut down

- over-give

- or cling to money like a life raft

Why?

Because those behaviours aren’t driven by logic — they’re driven by identity-level beliefs:

When those beliefs activate, the walnut brain takes over.

And the walnut brain doesn’t care about your spreadsheet, your plan, or your intentions.

Discipline works best after the identity layer is regulated.

Otherwise, you’re white-knuckling your way through a threat response.

Limiting Beliefs Commonly Linked with Anxiety Therapy

These identity-level patterns frequently show up for clients seeking anxiety therapy. Explore the beliefs to learn the “why” and how therapy can help you recondition them.

“I Am At Risk”

“I Am At Risk” is a core belief rooted in environments where safety felt unpredictable. It often drives patterns of anxiety, catastrophic thinking, and compulsive control.

Explore this belief

“I Am Not in Control”

When “I Am Not In Control” is running the show, everything feels like too much. You either grip harder—rigid routines, hypervigilance—or give up entirely. Underneath it all is…

Explore this belief

“I Am Falling Behind”

The belief “I Am Falling Behind” shows up as anxiety around progress, panic over timelines, and shame when comparing yourself to others. Therapy addresses the internal pressure and…

Explore this beliefWant to see how these fit into the bigger pattern map? Explore our full Limiting Belief Library to browse all core beliefs by schema domain and Lifetrap.

🎙 What We Cover in This Episode

1. The psychology behind financial overwhelm

Stress responses like freeze, fawn, or over-functioning show up easily around money — especially when identity beliefs are activated.

2. Why Calgarians feel “behind” even when they’re not

Calgary’s achievement-heavy, comparison-driven culture fuels timelines, pressure, and unrealistic standards.

3. Identity-level beliefs that drive money behaviours

Beliefs like “I am not in control” or “I am falling behind” quietly shape reactions more than any budgeting method ever will.

4. How avoidance keeps the nervous system stuck

Avoidance gives temporary relief — but compounds long-term stress, shame, and disconnection from goals.

5. How therapy + financial planning work together

Why functional change requires both emotional regulation and practical strategy.

💬 Key Quotes from the Episode

“People think they have money problems. They actually have threat system problems.” — Andrea

“The belief ‘I am falling behind’ is the engine of so many financial decisions.” — Jenae

“You can’t budget your way out of a belief.” — Crystal

Identity-Level Therapy for Money Stress

At ShiftGrit, we don’t treat “money issues”; we treat the belief patterns driving your emotional reactions to money.

Identity-Level Therapy helps clients:

- Regulate the nervous system before making decisions

- Recondition beliefs like “I am not in control.”

- Reduce shame, guilt, and avoidance

- Build confidence in long-term decision-making

You don’t need more willpower.

You need a new identity pattern.

Identity-Level Therapy for Anxiety

Identity-Level Therapy targets the belief patterns and emotional loops driving automatic reactions—not just the surface symptoms. By working at the identity layer, clients shift how they interpret safety, regulate threat, and relate to themselves and others. The result: reconditioning at the root of shame, self-sabotage, reactivity, and overwhelm.

It’s organized around three pillars:

ShiftGrit Core Method™

Our structured framework for breaking outdated identity patterns.

Learn More

The Pattern Library

Real-world examples of loops like perfectionism, procrastination, and shutdown.

Learn More

The Glossary

Clear definitions that keep the language sharp and the process transparent.

Learn MoreIf You’re in Calgary

Explore how structured, transparent therapy works at the identity level:

👉 Calgary Therapy: What Most People Don’t Know When Choosing a Psychologist

Jenae White, R. Provisional Psychologist – ShiftGrit Calgary

Profile: https://shiftgrit.com/therapists/jenae-white/

Crystal Taylor – Holden & Taylor Advisory Group

Website: https://holdentaylorfinancial.ca/about/

Instagram: @taylord_advisor

Explore this topic

Related concerns we work with at ShiftGrit:

- Comfort Spending & Financial Avoidance

- Always Reading Between the Lines

- Anxiety

- Doomscrolling & Digital Overconsumption

- Hypervigilance / Threat Sensitivity

More from The Shift Show

Episode transcript

Andrea McTague: All right, welcome back to The Shift Show. As usual, I'm your host, Andrea McTague, registered psychologist and founder of ShiftGrit, Psychology and Counseling. Today we are talking about something that every single person has a relationship, whether they want to or not, and that is money. And more specifically, why money feels so stressful, so emotional, so overwhelming, and so avoidant for so many of us, even when we technically know what we should be doing. This episode is called Mind Over Money, overcoming the limiting beliefs that keep you stuck. And we're diving into the psychological patterns that drive our financial decisions and how those patterns are shaped by limiting beliefs and what you can do to move towards clarity, confidence, values-based money choices. And we'll talk some strategies and some insights from two sides of the coin today. So I have two fantastic guests with me today. First, have Crystal Taylor. Crystal is a financial advisor and the CEO of Holden and Taylor Advisory Group. And her career began nearly two decades ago after a difficult early experience with insurance that completely changed her perspective on financial protection. So she entered the financial industry in 2006 and went through the 2008 financial crisis early in her career. So that must have been a wild, interesting shit show. And has since guided clients through every season of financial stress and transition.

Crystal Taylor: Thank

Andrea McTague: So we're very, very lucky to have her on the pod today. We'll get into it a little bit and her passion about building a healthier, more grounded relationship with money for her clients. And we've got Janaye White joining us and she began her career actually as a licensed financial advisor at Holden and Taylor before coming into the ShiftGrit ecosystem as a registered provisional psychologist and to participate in some brain bending over on our side of it. So she's seen both sides of this topic, the practical financial planning world and the therapeutic world. So she's worked through many of her own limiting beliefs around money, as I'm sure we all have, right, in that career shift. And today she helps clients identify and recondition the beliefs and the patterns that quietly shape in the background the way they approach money and work and relationships and a whole host of other stuff. So it's definitely a full circle moment where we've got Crystal and Janaye.

Crystal Taylor: Thank

Andrea McTague: from the financial world moving into a little bit of the intersection in our psychology and therapy world. And before we begin, just a quick reminder that this podcast is for information and educational purposes only. So it's not to be construed as financial advice and not a replacement for working with either a professional financial advisor or a licensed mental health professional. So if you need that, please reach out to either Holden and Taylor or ShiftGrit or somebody else. on that site and this is just for a little bit of education on the topic. So let's get into it. Crystal, we're going to start with you. Why is something as essential as money also one of the most avoided and emotionally charged topics, do you think, in people's lives?

Crystal Taylor: Thank you. think that money is a tool or like a double-edged sword. So people have had early life experiences with money that they may not be conscious that they're operating out of. They have societal pressures, family pressures, and then now we have added on top of that so much media pressure. So people are experiencing a bombardment of information and a lot of people, as you know, will choose to respond in one of three or four ways, right? The fight. flight, fawn, freeze. And there's so much life happening every day that it's pretty easy to just keep moving on to something different and letting things fester in the background.

Andrea McTague: 100%. So like lots of avoidance directors. You see that? Yeah.

Crystal Taylor: Yes, we see that quite often, heading the sound activities or passing the buck to a partner, those types of things.

Andrea McTague: So what originally pulled you into this field and what made you want to focus on like protecting and supporting people financially? Like where did that come from?

Crystal Taylor: I was a unique individual when I was younger. I was an athlete and so I grew up relatively quickly and I didn't really realize what was happening at the time but my parents were married young, had a young family and it naturally occurred in my life to become married young and have a family young and during the process of all of that I became a homeowner at the age of 19 which is highly unusual and I had owned my second or third home by the age of 21.

Andrea McTague: wow.

Crystal Taylor: So when we were buying that home, we hadn't quite had our child yet, but we were talked into some mortgage protection products with our lender. And we had never thought about life insurance. No one had ever talked to us about it before. We were so young, I was in university still. And so when we were told by the lender that you should have some life insurance on your mortgage and some criticalness and some disability, we were like, that does make sense. I mean, it wasn't. rocket science and I was married to an athlete. you know, was like, that's a great idea. And sure enough, not long after that, he was actually quite injured. And when we went to try to claim on this insurance for disability, that's when my whole world just came to a complete halt. We were expecting our first child. And I recognized that what I thought insurance was growing up in Alberta as a Canadian was not exactly the experience I was having at the lending level.

Andrea McTague: Yeah.

Crystal Taylor: And I happened to meet a person at this time in my life who was an insurance person, who was a licensed insurance advisor, had explained to me the difference between owning your insurance versus not owning a contract and all the ways that insurance works in Canada when you're protecting your life and your wellbeing. And I just dove in. mean, it must've been some young blind faith, but I got licensed to do insurance and I was gonna save everybody from. lending insurance and make sure they had really proper protection that would actually be there for them when they needed it. And here I am. And 2008, you further you mentioned 2008 when you were doing your introduction, you know, that further entrenched, I did not want to manage money. And all of a sudden, my phone was ringing because people didn't know what to do with their investments. And that just started me on the trajectory of money management. And then I was, you know, looking around at having investment money and insurance and you know, what are these things doing for you as a family and as a couple and as an individual who's earning an income and people didn't know how to, you know, put it all together. So that's when we became planners.

Andrea McTague: So yeah, and I definitely see that like the level of financial literacy is sometimes so low and financial products and insurance products can be so complicated that I think just the daunting nature of them and people feeling like they are stupid for not knowing or, you know, just even not knowing that you don't know, really, really, really common, right? And how do you find the people and deal with the stuff? And it gets so overwhelming for a lot of people. I think they just piece out. They're like, no, I'm not going to look into it at all.

Crystal Taylor: I don't blame them. Don't blame them. Yeah.

Andrea McTague: Yeah, it's a whole different, which is why I think it's kind of important to work with people that are professionals in that sense, because we all have our other thing that we do during the day, right, for our other job. So, but what part of the job do you love the most? Like, what do you enjoy about it the most?

Crystal Taylor: Completely. I love so much of our job, but mostly it's just deep relationships with people. They trust us with the most intimate parts of their lives because money happens to touch most of your life. And so when you develop that over time, because I've now been in this role for so long, when something happens really good or really awful, we have the ability to make such an impact and help them through that. that I feel like, and Janaye can probably attest to this, on the psychological side, they can actually work on the pieces that matter most in those moments, like grief or how do you acknowledge a windfall. Because that's actually quite overwhelming for people, but if you have a solid financial situation happening and you know where your money's at and you know what your plan is, you can actually go and understand that you're having to struggle somewhere and... and take that time that you need to address it and get some help.

Andrea McTague: Nice. 100%. Janaye, was this kind of your experience when you were working in the financial world?

Jenae: Yeah, it was wild to see the things that you got to learn about people's world and their inner workings and how it just affected the whole family and certain things like Crystal said, like an inheritance that some people might think, well, that's exciting minus the event of the death can come with a lot of guilt or shame or confusion or limiting beliefs about like deservingness of the money or wanting to like keep that money. And so it was quite an honor to see that as well as like the successes and the shifts in people's mentality.

Andrea McTague: Very interesting. I'm just going to get you to lean a little bit closer to your mic so I can hear you a little bit clearer. And then, so now you've had this unique experience of seeing it from that side, which obviously, first of you've been exposed to a lot of the emotions around money and the good and the bad. And so how has that been for you, Janaye, when you see it like now coming up in more of a therapy realm? Because it's not like the money topic went away. For you, it just changed the way you're helping people with it, I think.

Jenae: Yeah. I mean, I think the cool thing about this angle is when people are coming into a financial advisor, they're getting support with behavioral change to an extent if they're open to it, and they're getting like financial literacy in some of those pieces. But then there's like a subconscious part that really holds people back from doing the thing that they know they need to do. And so to be able to work with that piece, and kind of target the behavioral angle, the subconscious angle, all those money stories and see those shifts and see those shifts affect things other than money too in this really global way. That's what lights me up and is really cool to kind of target it in the therapy room as well.

Andrea McTague: Well, and it's an interesting one because I think all three of us really play with money a lot with clients in general. My particular client population is high net worth individuals or entrepreneurs and founders. And so the money issues in that space are crazy huge, both on what you were saying, Crystal, like the good side. Sometimes people not knowing what to do with a windfall. Maybe they've exited their business and they think, OK, well, now I've got this bank account full of stuff, but I don't know what I'm doing with it. I don't know where to put it, how to deploy it.

Jenae: Yeah.

Crystal Taylor: and

Andrea McTague: And then also, I don't know how to interact with family relationships with it. That's a hotbed of stuff. Or what to do with their time, right? So it's just a messy one. But also on the other side where there's that scarcity, cash flow issues, panic about it. know, I'm sure whenever there's word, that recession word comes into the news, everyone starts to lose their minds a little bit. So very, very, very interesting. Or just I think that we'll get into kind of some different profiles.

Crystal Taylor: Yes.

Andrea McTague: of what it looks, what the different issues around money look like. And we'll talk about why money messes with our heads basically. tell me a little bit then about like what, maybe Crystal you can start us off with. What are you seeing as one of the major, it's a couple of the major stressors that people experience with regards to money now in our current reality.

Crystal Taylor: Yeah, current reality is very different than when I started in this business. So we've seen things that other generations had not really experienced before. So some of the things that we've seen, we lived through a pandemic, which our parents didn't. So that was really interesting to navigate with people. And we're not equipped to deal with the psychological piece. And so sometimes the biggest hurdle for us is the math that we're showing can make such great sense. and then the behaviors will not match up. And so, and we have a hard time moving the needles. So we will often say like, maybe you need to go address, you know, why this is so hard for you to take this step. What's holding you back? Because we are not trained to go and dive into, you know, childhood experiences or, you know, other demographics that are going on in the background. We've also seen the fallout from the pandemic of inflation. And so people are afraid and they are

Andrea McTague: Yeah.

Crystal Taylor: you know, saying things like, want to hide gold in my basement. That was a meeting I had this morning because gold, yeah, because they're like, I know it will be there. And I'm really scared that like AI is going to wipe everything out. And then I'm just not going to have anything. And I've worked my whole life for this. And so it's a valid feeling. so telling people like, that's a valid feeling. We can understand why you're feeling this, but it's also not rational behavior. And so that's really tricky.

Andrea McTague: Very 1932 vibes. Yes.

Crystal Taylor: because we want people to be wealthy. We aren't, you we want people to do well with their money. And wealthy to me means that you're very, you're feeling confident about your money. You're not worried about your basic necessities and you know that there's some fun coming along the way as well. And so helping people like step into what their definition of wealthy is and understanding that it's not just a number and it's not comparative to other people is something that I think helps them through some of these. But of course, we're still working through the current scenario of what's happened and we're still struggling with confidence in our economy. So we did have an event last week with an economist and the feedback I've been getting is I thought Canada was in worse shape.

Andrea McTague: out.

Crystal Taylor: And so that made me feel really good for bringing that out to everybody because people were trying to exit all of their Canadian investment holdings and go purely, you know, US or global. And, you know, it was like not exactly the perfect move for most people, but they were just so afraid and the media is so hard to decipher. So that's, know, where we're at.

Andrea McTague: Mm-hmm. Well, and think you're kind of talking about something that I'd say like, Janaye and I both see a lot of, and just in general as well in friends and family, where it's this like reactionary thing, where people will go from an avoiding kind of construct where they're just like, I'm just gonna ignore it, I'm not gonna check the statements, to all of a sudden there'll be some trigger, whether it's something they heard in the media or whatnot, and then all of a sudden it's like, I got to liquidate everything. got to buy gold or I have to save. We should sell the car like just just over to the extreme. Are you seeing that, Janee and your client population as well?

Jenae: A little bit. Yeah, like as a general principle, kind of like the pendulum just swings like so far instead of these like small grounded adjustments if people are in that like freak out state and the information doesn't necessarily get in if they're that activated.

Andrea McTague: Well, and that's what we're seeing. Like, Jenea and I are both like big yoga people. So the yoga stuff taught me that it's really about sustained incremental progress and that discipline for those like tiny needle moves, which I think it translates directly to money behaviors, right? But when we get that swing from like the avoidance side of things to these reactive big move type of things, yeah, we're not going to see that progress because it's so intermittent and so kind of disorganized and chaotic. where I think that organization is really important. Janaye?

Jenae: And it's. Well, it still kind of avoids the situation to make this like one big dramatic panicky change because you're not really, really actually facing what's under it. And you're also probably not facing the small, difficult everyday decisions that are going to help you. You're just like, this will fix it. Like kind of like freak out instead of like, let me do the

Andrea McTague: 100%. I was talking to somebody actually the other day and she's got some major overspending habits and she's aware of this but continues to do it. But then something happened and she's like, okay, you need to tell me like how, like how do I save? How do I save money? And like, it was like, you know, in a 30 minute conversation, how do we save money? How do I stop spending like way beyond my means? And you're like, well, the thing about that is we have to go like backwards. And I think look at the underlying of like, why are you doing that in the first place? What is it linked to? Cause we see it tied to a whole bunch of different limiting beliefs, right? And then that head in the sand, ostrichy kind of stuff. But at the same time, then it needs to go into, you need to work with somebody to set up like some strategies and a plan so it doesn't become, and I think this is something that I see with clients is if it is about making a decision in the moment every day, that's going to be really, really difficult. But if you've got, yeah, and just not,

Crystal Taylor: See you

Andrea McTague: It's not going to happen. kind of say it's akin to, you know, going on a healthy eating thing or a diet, but you've got your like big jar of favourite cookies on the counter. You might pass by that 50 times, but the 50 first time you're like, ah, because maybe you're tired or maybe you had a bad day at work or whatever. So it has to be something that I think that is a little bit more of a structured plan that makes it easier to make the pro money decisions versus harder. and not have that stress all the time because we see a whole bunch of things getting activated.

Crystal Taylor: Well, compiling on that, though, is that pressure to DIY all of your investments and not pay somebody to help you. And the data is coming out now that people are really only netting about 3 % because they're making emotional decisions. They're not setting up automatic contributions. They're not making any adjustments. And they're not seeing the progress because they're not tracking it in a way that's meaningful. And so when they're up at 2 o'clock in the morning and they're afraid, they're like they're getting out of things that they shouldn't be maybe, or they're buying things that they shouldn't be.

Andrea McTague: Mm-hmm. Mm-hmm.

Crystal Taylor: in their investment holdings and so they're not making the traction but the way it's advertised is that because you're not paying the fee you're going to have all this extra money and that's just not what's actually happening.

Andrea McTague: Yes. And I've certainly been guilty of that myself where it's like, okay, I'm just going to manage all my stuff myself and I'm going to take care it. And then the thing is that's really cute in a week where, you know, you have the time or whatever and you're in a nice emotional state that's even, but you get into scenarios where then you ignore it, you get too busy. And then I think the big one also is that it's a full-time job for a reason, being a financial advisor. So if you're trying to do that full-time job on top of what is your

Crystal Taylor: Yes. Yes.

Andrea McTague: normal full-time job less crazy busy life. And I think that's something that we see across the board now, certainly in our client population, know, they've got the kids and then they want to do this thing and then they're going to like their Pilates class and like just all the stuff to manage life and then trying to squeeze it into that, 5 % of available room when it's there, it just creates a chaos structure. And I think just not having help humans do really well when we have somebody like walking us through things, setting things up with some knowledge, almost like a bit of mentorship, I would say you kind of feel like that sometimes with your clients.

Crystal Taylor: Yeah. We do. like in one of our events, we show a slide that I think is really important and it shows rate of return. And this is to get across the fee conversation. So let's say that there is a pack going in, they're paying monthly $100 a month and they're saving for this amount of time. And if they're getting a four, six, eight or 10 % rate of return after fees, the first few years look pretty boring on all of those returns. Right. And they don't really start to accelerate for a number of years. And so helping people stay the course because people will go up and set up a new account because they're like motivated. They've listened to a podcast or they've read something that just like got their attention or saw real or a Tik Tok or something that was like, yeah, I got to do that TFSA thing. And they'll start putting the money in and then, you know, six months goes by and they're like, I only have an extra like $30. I don't really need this. Those like those new earphones that like I saw.

Andrea McTague: This is stupid.

Crystal Taylor: They look way cooler than those 30 bucks and they cash it out. It's awful.

Andrea McTague: And I think like one of the things that I see also is when I talk about money with clients and they might not be, sometimes I've got clients with high financial literacy, those are usually your entrepreneurs just because out of necessity, you kind of have to figure out how to, you're like, I gotta make payroll, so we gotta figure out some of the stuff around that. And not necessarily always high financial literacy, but with a lot of my other clients, I see this belief that

Crystal Taylor: Survivor. Yeah.

Andrea McTague: Well, I don't have a lot of savings. I don't have a lot of money. So I can't like the financial advisors and things like that. That's for people with money. That's for people who've got a lot. And I think, you know, that when you're just getting started and Janay, you said something when we were talking a long time ago where you'd kind of come from a scenario where you're like, okay, well, I don't know a lot about this stuff. I don't have a lot of high financial literacy. And then you ended up working. that space. Do you want to speak to kind of how you got from the like, I don't know anything about anything about this and I'm not like, you know, raining down the denieros to kind of having that financial literacy and being able to make proactive choices.

Jenae: Yeah. Yeah. So I was a broke yoga teacher when I decided to take the job at Holden Taylor. And it was almost like because the thing I was doing that was so fulfilling emotionally wasn't fulfilling that financial need. I wanted to do a total switch and I did have a background in business. So it was like a pretty like logical transition that way. But it was just kind of like, okay, let's do the opposite of what I'm doing right now, because it's kind of not working. And then just through seeing different client scenarios across like all kinds of income brackets and lifestyles and like what worked in those scenarios, things that I hadn't necessarily thought of before, that sort of started to be inspiring. And also seeing just like the changes people were making to actually implement change myself was really cool. So yeah, the... The initial entry was kind of like, it's not working, let's do something different and I really want to get my finances in order. And then the staying and feeling really invigorated was those personal connections that Crystal was talking about. And then the leaving was not liking the admin and being so inspired by all of that connection and those behavioral and psychological pieces that I get to do now in terms of finance and other things.

Andrea McTague: So you're kind of like oriented to like, get into the psychological, but very, very interesting. And I think that that's a great like start, cause like I said, we see it where it's like, well, I don't have any, and then I'm embarrassed the shame structure around, you like you were very open about like, I was a broke yoga teacher. A lot of people have so much shame around that where they, or they've made dumb financial decisions or they feel like they've made a mistake or a dumb investment or something that didn't net. And then they don't want to tell anybody about that. And you know, I think that

Jenae: Yeah. Bye. No.

Andrea McTague: what you're speaking to with getting that social support is huge, not only for the support and the education, but also for the accountability, I would imagine.

Jenae: yeah, yeah, and like we had a lot of financial conversations in the office, obviously, so not from a place of shame, but there was a lot of accountability, because it's exciting to talk about the progress and it's exciting to hear what someone else is doing and if it's working to like implement that yourself.

Andrea McTague: Mm-hmm. 100 % when you start to see what's possible, it's very cool. Like I remember the first time like way back in the day, I was like, what's compound interest? What? It does this after 10 years? You know, like it's very, very neat stuff. So in terms of your client base, we've got an our client base, I think we see like overspending as a huge common, common, common one. Obviously, that one I think is more common is what people understand is like the

Jenae: Yeah. Yeah. Yeah. Yeah.

Andrea McTague: you know, buying the new AirPods or whatever when you're like, probably don't have the spare cash around for that.

Jenae: Yeah.

Crystal Taylor: But I also will say that I do see something that does happen naturally in couples with the overspending conversation that I try to shed light on. So often one person in a relationship, it's still more common for it to be the woman, but it's evolving, is the person who does all of the household stuff like the groceries, registering kids for things, getting the kids what they need for school, etc. And I will hear from the other partner, well, they spent too much.

Andrea McTague: the Mm-hmm.

Crystal Taylor: And so I often say, okay, well, what if we take out all of the things that all of you need to sustain life as a household? Is she spending or they or he like is the other person spending money that you think they could save somewhere along the way? Because yes, there is true overspending and true shopping addictions and those things need to be addressed. But

Andrea McTague: Yeah, yeah.

Crystal Taylor: I do find that sometimes the conversation is, it's shocking what we actually spend versus what we think we need to spend to survive our life or live our lifestyle the way it is right now.

Andrea McTague: So pairing it back to like, what are we actually looking at? Like what's actually realistic? Because it can't be like, you spend nothing. And then obviously there's that misinterpretation from one partner to the other. We see a lot of that in the relational dynamics for sure. And we actually play a fun little game called found money. We'll talk about that a little bit later to trick the walnut into looking at that. And it becomes a communication tool. But Janee, when you look at relationships, what are you seeing?

Crystal Taylor: Mm-hmm. can't wait.

Andrea McTague: in your client population or just like in general as a big friction point when it comes to money.

Jenae: It's actually like the parent-child relationships that I often find quite interesting. And so when I'm thinking of some of the clients that I'm seeing, something that pops out where I think people might be thinking of like scarcity in terms of money from like a perspective of not having enough being a real trigger is quite affluent people that their parents help them a lot. And two, limiting beliefs really popping out there is I don't deserve, like I haven't worked for the things I've done, even when in reality they've done some hard work and then I'm incapable because they've had this sort of like financial coddling. And then with that, some enmeshment with the parents where they're not making their own values aligned decisions. So there's that, that's like one dynamic that I see as a really primary.

Andrea McTague: Yes. 100%. And we're seeing more and more of that and probably more than we've seen in any generation, I think. And I often see it from, you see it from the child side, I see it from the parent side of how do I get out of this demented dynamic that I've made? Because now I've kind of, you know, given them the thing, like how do I stop doing that? Maybe they're 40 now and I'm still paying like half their mortgage and they can't extract themselves because they're worried like I'm at risk or I'm gonna be unwanted, they're gonna reject me, something like that sort of thing.

Jenae: Yeah. Yeah. Yeah.

Andrea McTague: And you were saying another dynamic that you see often in relationships.

Jenae: It actually ties into that because I'm blanking on the last name. There's a woman named Chantal that recently released this amazing book called The Trauma of Money. And she has coined this term financial fawning. And it just beautifully describes this dynamic where people are overspending, usually on others, for a sense of belonging and worthiness. And I think that is a little bit what those parents are doing. But then also that can come from the perspective of the person always like footing the dental bill or kind of like over gifting. And so just like working through those limiting beliefs and like that confidence and getting like that worth from other places. Yeah.

Andrea McTague: Hmm? 100%. I also see that in marriages, especially where one partner, and for me it's usually my guys, makes a lot more and they have kind of got into this enmeshed financial over-reliance kind of spoiling dynamic, which then makes them really resentful. But again, it's hard to stop it and loop it. And I think often the other partner that's receiving doesn't really understand what you were saying, Christos. They don't really understand on the other side how much they are actually spending.

Jenae: Mm.

Andrea McTague: or how much they are using, right? And there's kind of other pieces around that, particularly with the business owners of how much it takes to make them. And so you get a lot of complex dynamics in the relationship realm, definitely. And then in the personal side of things, I also see an odd one, I suppose it's not talked about as much, but I see this underspending scarcity construct. It's really common with a lot of my founders.

Jenae: Yeah.

Andrea McTague: especially if one of their non-nurturing elements was to grow up without money. then when they... Yeah, they just can't because there's a great thing about it. Like some people cannot save money and other people cannot spend it. And so they'll have this kind of demented perspective where maybe they've got, it could be millions in the bank, but will not be able to purchase things. And it just is this scarcity construct that becomes very anxiety inducing and hard for other people in their lives to explain.

Crystal Taylor: Wealth through frugality mentality.

Andrea McTague: Right.

Crystal Taylor: I it in the retirement realm all the time because you spend so much focused time on your finances acquiring your wealth and accumulating. And then when it comes time to deploy it, they pump the brakes really hard. And so one of the books that we read as a team in our office was The Psychology of Money by Morgan Hussle. He just came out with a new book, The Art of Spending, and it is exactly about this. And it's absolutely incredible. I dove in so deeply that I just...

Andrea McTague: lovely book.

Jenae: Ooh!

Crystal Taylor: I wanted to clear my calendar for a month because it was just exactly what the whole generation that's retiring needs to hear. And it's what people need to be aware of while they're saving for their retirement, that there is a time to deploy those resources. I remember sharing with a client that they could put their dream car into their financial plan and it only reduced their retirement outlook by a total of 2%, but they were already overfunding their retirement by twofold.

Jenae: and

Crystal Taylor: And so, and they still haven't bought the car to this day. It's like a dream. It's a thing they want. And now there's a diagnosis and it's like, if you don't do it now, you're never going to like, we work really hard and it's not materialistic to want the one or two things that bring us some sort of joy or fun or adventure. and they're different for everyone. You know, they don't have to be a material item, but they can be an experience. They can be, you know,

Andrea McTague: Yeah, we'll just go into some thanks.

Crystal Taylor: place where you, you in your home where you feel like you can do the yoga or do the meditation or just read a book by yourself. Like you can spend a little bit on these things, right? So yeah, it's really interesting because this book is really timely for this generation that's retiring right now.

Andrea McTague: time. I'm definitely gonna take a read of that because we see it so, so, so much. And I see it in my own family as well. It's a business family and switch to that. it's that mode switch I think is difficult for people. Like you said, they're in this accumulation, gotta work hard, be industrious. And then all of a sudden it's like, no, and we're not gonna have a bunch coming in. So now we're gonna output it. And I think that there's just, we see a lot of mental blocks there. A lot of like, I'm powerless, I'm not in control, I'm at risk.

Jenae: Yeah. Yeah.

Andrea McTague: those types of limiting beliefs popping up. And then what Janaye and I can go do and the rest of the team here is we can actually go in and just remove those limiting beliefs so we don't have that tied to the spending anymore, which I think helps a lot. The other thing, so we touched a little bit on that over-reliance on partners where we just see this kind of abdication of money stuff. And this can be an over-reliance and abdication based on... partnerships or just an abdication to like, I'm just not going to check the statements. I'm just going to put it on the credit card. Like major ostriching kind of stuff, which eventually bubbles up, right? But do you see that in both of your kind of client populations and in general?

Jenae: Yes.

Crystal Taylor: Mm-hmm. Yep.

Jenae: Absolutely. like, honestly, I've even been in that spot before of like, partially, I just don't like opening email, but like, you kind of just don't want to see like, has there been like the growth that I want to see? Or like, am I still in this spot that's like behind where I want to be? Right? Or those things of like, okay, I'll change the habit tomorrow. And I did a deep, deep dive on like my credit card bills going several months back.

Andrea McTague: Mm-hmm.

Jenae: It was so cool to see how it aligned with my values and didn't. And being able to, once I actually like looked at it line by line, like the very opposite of avoidance, super quickly was able to turn things around like consecutively for like months. And imagine if I had like faced that a little bit sooner.

Andrea McTague: Well, and I think that that's that thing is that moment of ownership feels really gross, right? When you're like, ugh, and whether that's in, you you say dumb thing to a friend or you're not looking at your spending or whatnot. But when you can face that moment of ownership, you're essentially putting yourself back into a powerful construct because you're like, OK, well, if I messed it up, I can also fix it. And then if you've got somebody helping you, whether it's on the psychology side or on the financial planning side, a lot easier.

Jenae: Yeah. Yeah.

Andrea McTague: but we sometimes have to pull out the limiting belief that's blocking that. And I think you touched on one right there, Janaye, was I'm falling behind is a really, really common one.

Jenae: Mm-hmm. Yeah, I was going to say I will fail, which is different wording of almost the same one. Yeah.

Andrea McTague: Yeah, 100%. And Crystal, do you see that in kind of some earth? Like, what does that look like, that falling behind kind of belief or I'm a failure? What does that look like in your client population?

Crystal Taylor: It's really interesting. People don't really know their values.

Andrea McTague: Mm-hmm.

Crystal Taylor: And so I've had people where I've encouraged them to bring all of their statements. And then I encourage them to tell them what their values are. And then we look at the statements and ask them if they think that those line up. And often there's an area where it doesn't line up. And then they have to do some hard work. So I love it when people are getting financial planning and psychological support because it's such a big complex. It's not, like I said, not just a numbers game because the numbers don't change the behaviors. So if people can be supported on both sides and have the confidence to go and get psychological support. And you know, when I started my therapy journey about 20 years ago, it was really because my parents were like something, you know, I was starting to go through a divorce and you know, things are not great in your relationship. We think you need some help, but we don't know how to help you. So we'll help pay for this. And it... took me years to realize how out of reach that psychological support was for people for many years. I think it's getting better and I think it's much better now. It's built into more employer benefit plans or health spending plans and it's also just more widely available in different formats so people can access bite-size help when they need it.

Andrea McTague: I think we've moved from the stigma of if you're going to go to therapy, it's because you're nuts or you're crazy or something's wrong with you into moving more into a mindset of psychological help or therapy can be used to create excellence and life enhancement sort of things. We're seeing that move a lot, but to your point, we're still quite ragingly expensive and I think the field actually has to do some things to change that. We're looking at some fun little things.

Crystal Taylor: Mm-hmm.

Andrea McTague: And I also think people don't know how it can help, right? So for instance, with what we do, because it's specifically tied to limiting beliefs, which essentially cause a bond between a stimuli, in this case, often money or debt or a credit card statement, and it ties to that limiting belief, which then becomes an identity statement. So we've got a very reliable method to get rid of the limiting belief, which then takes it from an identity statement problem, like I'm not

Crystal Taylor: Mm-hmm. Sure.

Andrea McTague: I'm not good enough or I'm a failure or whatever, whatever is going on in the back subconscious that's going to promote that block feeling. And we just remove that. And then you are back into your cognitive logical brain, which can then make sense of all the strategies and the information that are available in the financial realm. But I think until that is rejigged, it's often very hard for people to align their behaviors and their emotional reactions to the execution of whatever the plan is, right? That's why we're seeing that kind of gap. it fills in nicely.

Crystal Taylor: It's also why budgeting is hard for an advisor to actually help with because budgeting and spending, are behaviors. And if you're not willing to actually do the really hard work to figure out where your money's going, then you're not going to stick to any budget that I create for you because it's not going to marry to your values or, you know, your limited beliefs are going to get in the way pretty quickly. And that's why I struggle the most when people ask me for that kind of help, because it is, I know.

Andrea McTague: Okay. 100%.

Crystal Taylor: a deeper problem than just, you know how much money you make, you know how much your fixed bills are, there's something in the middle usually, where is it all going and I can't stop you. Right.

Andrea McTague: And I mean, I think the other thing which you mentioned is the tie between, and Janay, touched on this, the tie between values and money, right? Because I think people get in trouble when they want to spend the money on everything, like, you know, buy everything generally, unless you're maybe Jeff Bezos, and he's probably in the position to do that. But we had done some studies, looked at some studies on where does spending matter? And of course, it is very different for different people.

Jenae: Yes.

Crystal Taylor: Yes.

Andrea McTague: Right. But we play a little activity game here called deathbed priorities to look at what actually matters to people. So if you have like one day to live one year to live, like, what are you actually, what are you doing with your time? What are you, who are you spending it with? Because that question is hard to answer for a lot of people. Like, what do you really value? Or sometimes it's completely out of alignment. Like I was talking to one of my business guy friends and I said, well, why do you own the business? And why do you like, what's the money for? Like, why are you making all this money? And he thought about it he's like, well, we cut for freedom. And I was like, freedom to do what? And he's like, freedom to spend time as a young family. He's like, freedom to spend time with my family. And I was like, okay, so let me get this straight. You working like 80 to 90 hours a week is the answer to you spending time with your family, which is what you most, your highest value. Like, so you see these like massive contradictions, I think, when it comes to. money that impact lifestyle and all kinds of things, but you're like, that answer is just that he didn't know what he valued. There's something else there.

Crystal Taylor: Well, and I did start my career off very slow to be home with my child when he was young because I wanted to be a present mother and I did achieve that. It came with sacrifice, but I knew exactly why I was doing it. Sometimes a kid is really a powerful motivator and sometimes you think you have more time with them than you do because now that my son is 19, I know that that went by very quickly. And so I was intentional about it.

Andrea McTague: 100%.

Crystal Taylor: And that was my value at the time. And then when he all of a sudden he was grown up, it had to shift like now what are we doing all of this for? Right.

Andrea McTague: Well, and I think that keyword is intentionality because we always play with the construct that there's kind of two minds. You've got your evolved cognitive brain, which is great at like strategic execution, delayed gratification, all that stuff that's very, very handy for the modern world. But on the other side, we have what we call the walnut brain or a K like threat brain. And he doesn't do any of that. So that's a great realm of like impulse spending or inability to say like a lot of these money snafus come, I think, out of the walnut. taking over and driving things. We definitely see that I'm falling behind one, popping in. Let's talk about a couple different profiles of different money issue personalities or whatever you want to call them. So we've got our supersavers. Let's start with them. What are we seeing for beliefs and behaviors and problems and things in this supersaver realm?

Crystal Taylor: sure.

Jenae: Yeah.

Crystal Taylor: I love it.

Jenae: Definitely I'm at risk, a little bit like not in control. Sometimes it actually comes down to worthiness because their net worth is their worth and sometimes it comes down to deserving this. Like I don't deserve to sort of like have these things, all the money is getting saved but they're actually not getting to have any of the.

Andrea McTague: 100%. I have a joke with my dad because he would be in this category about, I'm like, hey, did you stop by the Merc dealership on the way home? Because he's done very, he's one of those like rags to riches immigrant stories. He's done very, very well, but it's a joke because he would never ever buy something that he would deem as like a luxury item for himself, despite being in the position of like, why not now? Because, know, he was older and stuff like that. So, and then I think what you're saying also, the I'm at risk one where it's just like a, like a.

Jenae: Yeah. Yeah. Yeah.

Andrea McTague: If I do it, then it's gonna be gone and there's not gonna be anymore.

Jenae: Yeah. Yeah, which is interesting because you even see that in billionaires and so they're like literally not at financial risk, but let's hold on to it. Like there's a dysfunctional need right there.

Andrea McTague: 100 % excellent. Well, I was talking to one of my other friends and he's terrible with money, never has any. comes out of his fans as fast as he gets it. Super saver. And he was talking about, well, you know, rich people, blah, blah, blah. And I was like, no, no, wealthy people often have this one where they don't spend. And I was trying to explain to him that that's often why they are wealthy, but it can overcorrect to a crazy level. So, Crystal, what are some of the things that you set up in that realm? If you've got these super saver, can't spend scarcity.

Jenae: Yeah. Yeah.

Crystal Taylor: The super savers, saving and investing are different things, right? Saving is like immediate access. You're not going to put it at risk. And I do find people when they are of a super saver mentality, they are often missing out on a lot of potential as well in the markets because they have way too much in savings. And so we'll say, okay, if you need an emergency fund and it's one year like to be like really aligned with the things that you feel, what does that amount and why then do you have all of this money just sitting? in a cash situation. And so, you know, I remember my dad's similar story to your dad. His retirement gift to himself was his new truck. And it was at a time when it was really hard to get one in Canada because they were all going down to the US. And so my mom had called me and my mom never swears. And she's like, go with your dad to the dealership and don't come home without a bleeping truck. And I was like, okay. And we found one at a small dealership just outside of Calgary.

Andrea McTague: You're like, okay, this is big deal.

Crystal Taylor: And you know, we took it for a test drive and the guy said, you know, someone's in the financing office right now, but we don't think he's going to get approved for it. So if you want it, just let us know. So we're on the test drive and I said, you know, it does all of the things that you want it to do so that you can go on these adventures, do all the things. And then when it came time to buy it, my dad just turned white. I know. And it was so hard. Yeah. It was so hard for him to do that because he wasn't quite raised for riches, but he was, you know, a really hardworking father of three.

Andrea McTague: Yeah, was activation.

Crystal Taylor: and you worked until you were this age and you retired and your pension was going to do these things for you, which has evolved a lot for people. then, know, so it just really was a big shift. so we see it like with retirees and we see it also with like people who have been left behind because their partner has left or their relationship has broken down or their partner has passed away. And so they'll like really clutch onto money and just be so afraid to deploy it.

Andrea McTague: it's almost like a comfort blanket. And you could see in that moment him switch from his cognitive mind into that like threat brain, like a tiger is gonna come at me, which is interesting. Then I think like the workaholics and stuff like that, like my friend that I was mentioning in a similar sort of thing, not being able to deploy any money for joy. But then we've got probably what I see more commonly in my client population and a lot in my friends. And that's the total opposite.

Crystal Taylor: Yeah. yeah, it was instant. Yeah.

Andrea McTague: the over givers, the spenders. So let's talk about the spenders, the ostriching, the ones that run it really close to the line, get into the debt thing, and then have eventually that panic moment, which I saw a lot of happening when they were raising the interest rates. And they're very, very leveraged and they're like, damn, like now I got a problem. So what are we seeing in terms of like beliefs and behaviors and things like that? And then what do you kind of do with the super spenders?

Crystal Taylor: Mm-hmm. spenders are tough. remember asking a couple early on in our journey together with them as clients if their interest rate doubled on their mortgage what they would do and they laughed at me and said it would never happen. Their interest rate was 2. something percent. I said it did happen and it was very quickly that the other party was back to work but then they struggled with child care costs and you know it was very damaging behavior.

Andrea McTague: We. Bye.

Crystal Taylor: And so I always just try to have conversations with people to buffer in changes that they can't control or foresee and make sure that they know what the plan would be. If your interest rate goes up and you can't afford your mortgage payment, your next logical step would be to, the other person gets a job, sell the home, are you willing to do these things? But you know, it bubbles up a lot when a relationship breaks down or a person passes away. When a relationship breaks down, we don't really have insurance for that.

Andrea McTague: Thanks, my friend. Mm-hmm.

Crystal Taylor: So navigating that really tricky scenario when there's not a lot of assets to divvy up, but you're divvying up a lot of responsibility, it makes it really hard for that, you know. Yeah, exactly.

Andrea McTague: And your costs double often, right? Now you've got two households, you've got two things to pay for, and often you're splitting liabilities as opposed to assets. We see this as a major stressor with a divorce scenario, which is just skyrocketing.

Crystal Taylor: Big deal. Yeah. And then we see it when we lose a partner, disability or passing away and, you know, not understanding how your employer disability is on your side or not. One lady, I met her after her husband had had a major stroke and she said to me, you know, what you don't know is how much the gap between what he was making and what his disability at work covered is. And I said, you would have if you were a client of ours, because we always talk about that. You know, let's just look at your plan and make sure.

Jenae: No.

Crystal Taylor: Okay, if you can't work, here's what you're gonna get. Is that enough for your family? What are the next steps that we're gonna take? Or are we gonna insure for the gap? And so if someone passes away, same thing. A lot of people are relying on things like lender insurance or employer insurance, and it's often way too little or unreliable.

Andrea McTague: Which makes sense. it's essentially like putting into what the senders having those difficult conversations. And I know, Janay, you and I are both therapists that are very interested in having the conversations directly about money. And sometimes it's raising this, sometimes our client raises it, right? Because they come in in a panic about whatever, whatever. But do you broach those topics from a psychology perspective with your clients? Janay? Yeah.

Jenae: me. yeah, I mean, I always even ask right in the intake about kind of like how finances were for people when they were growing up and what their relationship with money is now, because that pattern is going to show up in other areas as well. And then yeah, like down the line in therapy, if they are bringing up something painful like that, we've got that value of truth over comfort. So I am going to draw it to their attention and then give them a choice of like, Is that an area that you want to focus a bit more? And I do get a lot of clients coming in specifically because like impulse control is an issue. And so super spender impulse control, they often kind of like go together. And so we work with that from a learning belief perspective and like a habits perspective.

Andrea McTague: Well, because I see the comfort spending is what I would call it generally, as a really, really common opt out in the patterns where you can get that little hit of dopamine. A lot of my girl clients, we joke about like the home sense runs that you're like, I don't need anything, but I'm just going to go there and like spend a whole bunch of on nonsense. So it's that comfort spending, that little hit of dopamine. Um, and usually to fix that, are not actually playing with money at all. We're playing with getting other sources of dopamine that are not opt out.

Jenae: Mm-hmm. Yeah. Yeah. Yeah.

Andrea McTague: Right? So what are we missing? Are we missing like social connectivity? Are we a little bit overwhelmed, a little bit overburdened and what's causing that? And we go back and rejig that and it takes out that need to switch into the walnut brain that's gonna do these impulsive things and, you know, just put it on the credit card and so on and so on. So when we are realigned that again, put some more into their developed evolved cognitive mind, which then can digest some of the strategies around money or just not go there. Right? We also see like the realignment of these automatic responses that they just don't come up. You know, when we see comfort opt-outs in all kinds of areas, whether it's food or whatnot, which also kind of goes into the spending thing as well. Because when we get, I had one client, I was like, just for fun, let's go look at your thing. I just want to see Uber Eats, Skip the Dishes, DoorDash. Like, what's the total of that? And then let's just time that by 12. it was amazing. And she was like, Oh my God. I was like, yes, and obviously this is a very uncomfortable moment, but we're going to look at this is what the price of comforting rather than addressing the underlying issue is. And I was like, and also next time you think therapy is expensive, watch me get rid of this for you. And there you go. We just paid for ourselves. Right? So we've got that one a little bit. And I think that that spender thing, and also I think that there's a realistic piece in this, in this spenders and over spenders thing. A lot of people just

Jenae: Mm-hmm.

Crystal Taylor: yeah, yes exactly. It's brilliant.

Jenae: Yeah.

Andrea McTague: really, really close to the line now between inflation, maybe some job disruption, the economy is kind of like a bit funny in certain sectors and things like that here where they are really 100%.

Crystal Taylor: Pressure. Right? Even being a woman, like I look at what it costs for me to show about work versus my business partner who's a male. Like just my hair alone versus his, and I don't even have fancy hair. And you know, it's just, it's really, there's a lot of pressure. We're also online a lot. So things like I remember having a person who was really struggling with their month to month budget and feeling like they were living paycheck to paycheck. They were spending $800 a month on their injectables in their face, their brows, their lashes, their nails, and didn't feel like they could give anything up. And this was a person that worked in healthcare and it was heartbreaking. She was under 30 and this was like what she was burdened with, just feeling all the pressure to do all of these things. She's like, I have to do this to prevent the wrinkles.

Andrea McTague: Well, and it's something that I think is like a massive effect. You're seeing the financial effect of social media. Huge. Well, it's become a norm. Mm-hmm. Mm-hmm.

Crystal Taylor: Yes. Yeah. It's really big because, the pressure for supplements. mean, here you have this collagen, you have the like the fiber supplements now, like fiber is a big hit, right? And then now we're having like, women should also be on hormone replacement therapy, but it's not really mainstream. So we have to go spend money to figure that part out. And it's really, really tough to say like, what's actually going to get me what I need in the moment. And I dabble in some of it, but yeah.

Andrea McTague: And a class of necessities, right? Like these are going to the necessities thing and you have to kind of the conversation with people about is it not, like what is actually gonna make you happy? And are you exposing yourself to like things and realms where if you just didn't, like if we stayed off Pinterest, maybe we can just put normal Christmas decorations up and we don't have to go like, you know, to the crazy realm of making it look like this or that or that. So that pressure piece. Janaye, you talked a little bit about the over givers.

Crystal Taylor: Hmm.

Jenae: Yes.

Andrea McTague: Yeah, talk to me more about those ones, because that's the thing. And I think there's a great book, The Coddling of the American Mind by Jonathan Haidt. it talks about, yeah, great, because we are seeing so much of the hat. Talk to me a little bit about The Overgivers. Eliminating belief bias.

Jenae: Okay.

Crystal Taylor: Very good.

Jenae: I mean, the over givers, it's usually coming from a place of like, I'm not enough, or I'm not good enough, or maybe even that little piece around like safety. So kind of almost like buying that sense of worth and belonging. And if it's over giving, that might look like picking up the dinner bill for like your entire group of friends when you actually can't afford it. Like if you can afford it, and it's aligned with your values, that's super different. or kind of just feeling like you have to like buy your place in life or like buy your love. And it tips even a little bit sometimes into that workaholism or undercharging for your services if you're in sort of like an entrepreneurial space. And then a lot of times another limiting belief that will follow that or any of the overspending ones is then I'm irresponsible, which makes you just feel worse about yourself because now you're this person that can't spend, that does spend. and you feel irresponsible for it.

Andrea McTague: Well, because the dysfunctional need for I'm irresponsible is I need to be responsible for everything and everyone, including other people's emotions and reactions. Yeah, that one's a huge one around money. And I think it's actually quite ironically funny. I see I do not deserve in therapists often. Yeah, because we are in a helping profession and there is still this kind of misnomer that you can't help and deserve payment for that help.

Jenae: Exactly tons of overlap.

Andrea McTague: And Janay's heard my rant about this before, where as long as you are providing actual value and fixing the thing in the wild that the clients got going on, then definitely, and it's a bit of a modeling, but it's an interesting one with the over givers because they can kind of justify the spend a little bit easier because it's not for them, right? It's for somebody else. We kind of have to get into that a little bit.

Jenae: Yeah.

Andrea McTague: And then another really, really, really common kind of one, and I'm sure because we see a ton of this, is those avoiders. And I'd say this is actually the majority. This is the biggest thing that we see. say that the big chunk. Talk to me a little bit about these avoiders. What does that look like in terms of financial behaviors?

Crystal Taylor: Yeah. avoiders will do other things to distract themselves from what they should actually be doing. They don't want to open their statements if they're in the mail. Even if they're an investment or saving statement, they don't want to open any of it. I hear a lot of like, I'm dumb, I can't read this. I don't understand this. The minute they see it, they're just already overwhelmed by it. So they cannot logically see what's on the page. And sometimes those statements are awful. So I don't blame them. They're just not well formatted and clear. And so I always say to them, you need to

Andrea McTague: Mm.

Crystal Taylor: spend time every week, just a few minutes. So like have your favorite coffee, like even if you have to, I don't believe in the latte factor. So like you have your favorite coffee and then you open your banking app and you look at your, you know, your past 30 days, you look at like, have you made your credit card payment? Is it set up? So at least the minimum is going to be paid so that your credit is protected and just taking like little bite sized chunks to start getting comfortable doing these things because And I think people have this false idea that we are perfect at this as well. we're not, financial advisors actually have bad credit because they know how to ride the line. There's like a lot of financial, I know people that work at car dealerships and they're like, man, when you guys come in for car loans and it's not great. And I'm just like, sorry, I'm sorry. When I go and I do know my score, but it took me a long time to train myself to.

Andrea McTague: No. Hahaha!

Jenae: you

Crystal Taylor: to be comfortable with that because early on in my life, I actually had a lot of money and it was earned by my spouse and we were not in a great relationship, that's why we are divorced, but I wasn't allowed to touch it. I didn't deserve it. And I had grown up with not my immediate family, but extended family where any gifts and everything else had strings attached to it. So there was no unconditional anything. So I had to work with my therapist a lot on the strings attached to the money.

Andrea McTague: Mm-hmm.

Crystal Taylor: and how I can give as a person, because I actually do love to gift. And sometimes I'm an over-giver, like when Janaye says some of that behaviors, like, that's me, like the bill will come to dinner. And I'm just like, I'll just pay it because I don't want to have the conversation about like how we split it up or do whatever. But also it's not a place that's going to harm me because I'm also more aware of my plan. So I already know that my savings is automated, that there are certain things that I'm doing that are going to get me where I want to go. So I can. Yeah.

Andrea McTague: and offset that kind of plate maybe a little bit, right?

Crystal Taylor: Exactly. And I also like didn't get to have as many kids as I wanted. So I love to spoil my nieces and nephews. And so, but I do have to like talk to my husband, my current husband about like what we're doing, you know, because he'll help me and he'll be like, that's a little too much. Like that's a little too far, you know? And we have a really different money set up in our house that works for us too, where we're like, our finances are completely separate. We each have our own businesses and we talk about money and we know what bills we're paying for the household together.

Andrea McTague: There, wears the line. Yeah.

Crystal Taylor: but we don't critique each other. We trust each other.

Andrea McTague: And I think that's one of the interesting things is whether we're talking to clients that are, you know, on the beginning of that journey, maybe they're moving in together, maybe they're getting married, or ones where they're too in each other's stuff, there's too much enmeshment, how you can, the different ways you can set it up of like completely together, a little bit together, completely separate, and then aligned to those values, and the structure and dynamic in the particular relationship. And we get into that a little bit as well. Jenny, what are you seeing in terms of that?

Crystal Taylor: Okay.

Andrea McTague: side of things when it comes to the money showoffs. primary limiting belief. I am less than, right? I am inferior. And then they're going to be looking for societal markers to demonstrate certain things. What are you seeing in that? And I'm going to blame this. I'm going to say there's more of this in Calgary, in my opinion, than Edmonton. Yeah.

Jenae: Woo!

Crystal Taylor: Mm-hmm.

Jenae: Yeah.

Crystal Taylor: would agree with you there.

Andrea McTague: Edmonton seems to have a little bit more. And it's not that it doesn't exist here, but it is definitely a feature of Calgary's dynamic, we'll call it, social dynamic.

Jenae: Yeah. Yeah, I mean, those people like they're spending, but it's like they want people to see them spending. So it's more about spending on the thing that they are less about spending on the thing that they value, and more about someone seeing them spend on the thing. And then there's like socially prescribed things that are like the cool thing or the fancy thing. So they're buying these things. that they don't even like or want. Like they might actually be way more proud of themselves, and this is a biased thing, for like spending a hundred bucks on like a climbing membership, right? But instead they're spending a hundred bucks on like one glass of wine or something. And they're like, they can't even tell the difference. The Samoan couldn't tell the difference. But here they are living so far outside themselves.

Andrea McTague: Yes. It's a taste of the cross thing, isn't it? Well, and I have a client like that, we've had several clients like that, where when we start to remove the limiting beliefs of things like I'm worthless, so I need to be validated, I'm less than, so I need to be superior or whatever, we start getting these ones out that have to do with like status and from an evolutionary psychology perspective, status is very important for humans in group because if we're not at the top of the little monkey chain,

Jenae: Hmm.

Andrea McTague: then we're going to get less mangoes to eat. So it could go into a bit of a risk factor and starve. So once we get rid of those though, they're able more to align to what their actual values are and what the spend should be on or shouldn't be on versus the little as my bestie calls it, like the label whore constructs. Where you're just like, look at my bag, look at my thing, look at my whatever. But yeah, that's an interesting one that we would definitely see around. And it often puts people in weird financial situations because they'll go above and beyond to.

Jenae: Yeah. Yeah.

Andrea McTague: and like debt above and beyond to get into. Yeah, you're just like you're that Mercedes that you can't afford that's parked in the back there.

Crystal Taylor: Yes.

Jenae: Well, they're trying to outdo themselves at the end of the day too. So it starts off kind of medium big and how can you show off even more?

Andrea McTague: Well, it's almost like any sort of non-logical addictive behavior, it gets worse, right? Typically, because it doesn't stick and it doesn't freeze. then also the comparison structure is that there's someone always that's more and has more and whatnot, right? One of the things that I work on with some of my clients, and one of my favorite clients on the entire planet, this is one of the things that we're talking a lot about, is that lack of financial literacy being the barrier to getting any financial literacy.

Jenae: Addictive. Yeah. Yeah.

Andrea McTague: Ironically, you may talk to me a little bit about what you see, Janae, on limiting belief land, and then what do you see, Crystal, in terms of like those behaviors or what kind of strategies or information that you have for. getting those people in. we take broke yoga teacher, Janae version. One thing about you Janae is you are such, you seek information so openly without anything, but a lot of people, if they're in that situation, that's not the case for them. They want to hide and kind of mask their lack of knowledge, which of course then means that you never get any.

Jenae: Yeah. Yeah, so I identify as an ex-avoider, which is slightly different than these people that believe that they're like financially illiterate. But in those people, it's almost like shame is one of the core emotions. They're ashamed to tell the professional what they don't know. They maybe don't even know what they don't know. And some of that shame is often tied to their financial history, whether they come from affluence, poverty or somewhere. like in between and either way, you know, if somebody's like very affluent, oftentimes they're like, well, I'm like incapable. I've like never learned this. I should know this because like I grew up around money or if someone comes from less, they're just like, well, I'll never get there because I've never seen that modeled to me. And so it's interesting because like those things can start to overlap from a limiting belief perspective. But the way in of treating the limiting belief is really the same regardless of where it comes from.

Andrea McTague: 100%. Crystal, what are you seeing in terms of like, or what can be done to get those people kind of and what information would you give to somebody who's like, I don't know anything about money. I just feel dumb about it. It just, I'm not there. I'm never gonna be there.

Crystal Taylor: Well, it came up earlier, but there's a lot of pressure in our industry to set a minimum amount that we need to manage for you financially before we can call you a client. And so I've worked really hard to abolish that here and to make it about engagement. So I would say to you, hey, that's okay that you don't know anything about money. I actually don't think it should be taught in school because I don't really. think that children are capable of comprehending the reason that it matters so much. think sometimes a little bit of life experience teaches us to really care about something. And money is one of those things, right? And we can learn a lot by our parents' behavior, good and bad. And we can, if we want to acknowledge it, get some help around that and deploy ourselves as an adult. So if you don't know everything, that's okay. I have millionaires that don't know what a tax-free savings account is. I have millionaires that don't have a will because...

Andrea McTague: Mm-hmm. 100%.

Crystal Taylor: No one's ever explained to them the implications of not having a will.

Andrea McTague: Well, and I was saying to one of my multimillionaire clients who doesn't know a lot of stuff that you're like, are you aware of this? And he said the best thing to me, he said, it's kind of like when you've met somebody at a cocktail party like six, seven times, and it's almost like it's too far along for you to ask what their name is. And that's kind of the feeling that he's expressing. He's like, obviously I should know this, but now I feel dumb. Not.

Crystal Taylor: Yes. Great. Yeah.

Jenae: Yeah.